As the transition away from LIBOR progresses and the UK Financial Conduct Authority (FCA) has recently announced that publication of 24 LIBOR settings has ended, the FNG team has reviewed how major Forex and CFD broker have acted in response to the changes. In fact, a number of leading online trading companies, such as IG, CMC Markets, FOREX.com and OANDA, have taken action to inform their customers of the changes concerning IBOR transition.

- OANDA:

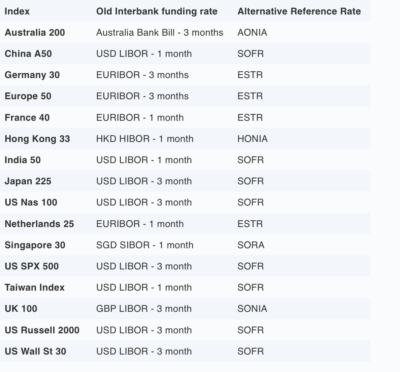

OANDA has implemented changes in response to the transition away from old rates back in November 2021.

The table below shows what each index product uses currently as its applicable funding rate and which Alternative Reference Rate OANDA has been using starting from 29 November 2021.

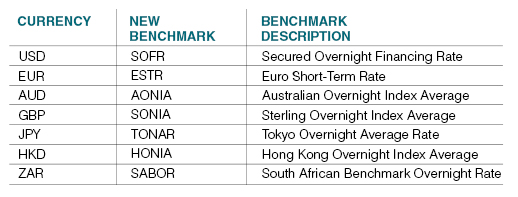

IBOR users are switching to Alternative Reference Rates (ARRs). ARRs are based on actual overnight interest rates in liquid wholesale cash and derivative markets. This makes ARRs more robust and less volatile than IBORs.

Since ARRs are risk-free rates, they don’t incorporate the credit risk that is inherent in the calculation of IBORs, which are based on interbank lending over longer time periods.

If you hold an index position at the end of the trading day (5pm ET), the position is considered to be held overnight and subject to either a financing charge or credit to reflect the cost of funding your position (in relation to the margin utilised).

On an index, this is calculated as:

Daily financing charge or credit = value of position* x applicable funding rate/365**

The applicable funding rate in this example will change from an Interbank Offer Rate (IBOR) to Alternative Reference Rate (ARR). For example, on the US Wall St 30, your applicable funding rate would change from USD LIBOR – 3 month to SOFR (Secured Overnight Financing Rate).

- FOREX.com

FOREX.com and City Index, which are now owned by StoneX, have also taken early action in response to IBOR transition.

If you hold a short-term trade and want to keep it open overnight, you’ll be charged a daily interest fee.

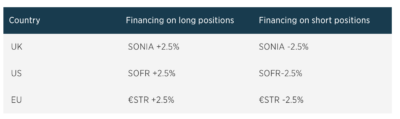

The financing charges reflect the cost of borrowing or lending the underlying asset and are charged at LIBOR (or equivalent IBOR) +/- 2.5% on the total value of the position.

Since 7 May 2021 clients of FOREX.com have been charged a rate approximating to the new benchmark +/- 2.5%. These charges will remain competitive in order to keep the cost of trading low.

- CMC Markets

CMC Markets explains that LIBOR has been replaced by a new interbank rate for the following currencies: GBP, USD, EUR, CHF, JPY and SGD. The table below shows the new interbank rates. Overnight holding costs will be charged based on the new benchmark rate, plus or minus our fee depending on whether you hold a buy or sell position in an index, share or share basket. Based on the new benchmark rates compared with Libor, CMC Markets does not expect a material change in holding costs.

- IG UK

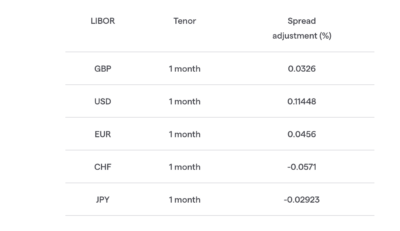

To compensate for the missing credit risk, IG has adjusted the ARRs by the one-month spread adjustment proposed by the International Swaps and Derivatives Association (ISDA).

IG used IBORs for the calculation of overnight funding charges on index and share positions. These have now been replaced by an ARR and a spread adjustment, meaning you’ll be charged fees according to the adjusted ARR benchmark +/- an IG admin fee.

- ThinkMarkets

Online trading company ThinkMarkets has announced new overnight funding benchmarks.

As of 13 December 2021, the broker has changed the interbank benchmark rate used to calculate overnight interest. This is due to a number of current Interbank Offered Rates ceasing to exist, including London Interbank Offered Rate (LIBOR).

ThinkMarkets will be replacing the current LIBOR benchmark with new benchmarks.

гостиница приморская санкт петербург

санаторий надежда анапа цены на 2021

санаторий в кабардино балкарии

кэшбэк 20 по карте мир условия

отель грейс глобал конгресс спа адлер

пицунда абхазия пансионаты и санатории цены 2021

куда поехать с собакой в подмосковье

санаторий крым в партените официальный сайт

парк отель европа в белгороде

отель камелот калуга

анапа бфо

артековская тропа

троицк гостиница центральная

дельфин оператор официальный сайт

санаторий в нальчике долина нарзанов

санаторий дубрава московская область официальный сайт

рябинушка отзывы

санаторий барнаульский цены

гостиница золотое кольцо владимир

курорт янгантау цены на 2021

отель морской уголок алушта

санаторий южный ялта

куда пойти в сочи в ноябре 2021

гостевые дома ольгинки

отель кристалл адлер

гостиница ангелина москва

отели в крыму 2022

санаторий крупской евпатория отзывы

санаторий солнечный берег геленджик телефон

отдых в бжид

санаторий нива саратовская область официальный сайт

отель аквалоо

гармония луховицы

санаторий целебный ключ ессентуки официальный

гостиница шелковый путь санкт петербург официальный сайт

санаторий горный воздух лоо отзывы

лермонтово 1

пошали брянск

санаторий нива анапа

детские курорты краснодарского края

гранд оазис

пансионат шаляпин кисловодск официальный

отдых должанская

pyatigorsk hotttt com

санаторий форос официальный сайт цены

очищение организма в санатории

во сколько обойдется отдых в абхазии

санатории в крыму в октябре

красная пахра пансионат

хостел новомосковск

ритц карлтон отель

златоуст гостиница

гостиница белозерск вологодская область

отель лоо сочи

санаторий исток в ессентуках официальный сайт

кисловодск санатории мвд россия

гостиница текстильщики москва

отдых в затоке

отели и пансионаты краснодарского края

санаторий лермонтова пятигорск отзывы отдыхающих

отель престиж центр питер

отели сочи меркури

пансионаты сочи

санаторий центр союз

отель надежда рязань

снять гостиницу в сочи у моря

гостиница гавань реж

парк инн бай рэдиссон саду

крым свадьба

гостиница мичуринск в мичуринске официальный сайт

хаятт ридженси петровский парк

гранд астория отель 3 россия феодосия крым

вилла алина

отель ока нижний новгород

аквалоо краснодарский край

бревис сочи

ржд мыс видный

вишневая гора в саратове

подмосковные парк отели все включено

отдых в ялте 2021 отели с бассейном

I m going to bookmark your web site and maintain checking for brand spanking new information.

Comment savoir avec qui mon mari ou ma femme discute sur WhatsApp, alors vous cherchez déjà la meilleure solution. L’écoute clandestine sur un téléphone est beaucoup plus facile que vous ne le pensez. La première chose à faire pour installer une application d’espionnage sur votre téléphone est d’obtenir le téléphone cible. https://www.xtmove.com/fr/how-to-know-who-my-husband-wife-chat-with-whatsapp-how-spy-another-phone/

Наша команда профессиональных исполнителей готова предъявить вам передовые системы утепления, которые не только обеспечат долговечную покров от холодильности, но и преподнесут вашему коттеджу модный вид.

Мы трудимся с современными средствами, подтверждая долгосрочный период использования и замечательные результаты. Теплоизоляция наружных поверхностей – это не только сокращение расходов на отоплении, но и забота о экологической обстановке. Энергосберегающие технологические решения, каковые мы осуществляем, способствуют не только своему, но и сохранению природы.

Самое главное: [url=https://ppu-prof.ru/]Утепление фасада цена за кв м[/url] у нас начинается всего от 1250 рублей за м2! Это доступное решение, которое превратит ваш резиденцию в действительный комфортный уголок с минимальными тратами.

Наши труды – это не исключительно изоляция, это постройка поля, в где все деталь отразит ваш персональный моду. Мы примем во внимание все ваши потребности, чтобы осуществить ваш дом еще еще больше дружелюбным и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]https://ppu-prof.ru/[/url]

Не откладывайте дела о своем корпусе на потом! Обращайтесь к квалифицированным работникам, и мы сделаем ваш обиталище не только тепличным, но и более элегантным. Заинтересовались? Подробнее о наших делах вы можете узнать на веб-сайте. Добро пожаловать в мир гармонии и качественного исполнения.

Наша команда квалифицированных исполнителей завершена предлагать вам передовые приемы, которые не только обеспечат устойчивую охрану от холодных воздействий, но и подарят вашему жилью трендовый вид.

Мы работаем с самыми современными материалами, обеспечивая прочный продолжительность службы и отличные результаты. Изоляция наружных поверхностей – это не только сокращение расходов на обогреве, но и заботливость о окружающей среде. Спасательные методы, каковые мы претворяем в жизнь, способствуют не только дому, но и сохранению природной среды.

Самое основополагающее: [url=https://ppu-prof.ru/]Сколько стоит сделать фасад дома с утеплением[/url] у нас открывается всего от 1250 рублей за квадратный метр! Это бюджетное решение, которое сделает ваш жилище в подлинный тепловой корнер с минимальными затратами.

Наши достижения – это не только утепление, это постройка территории, в где всякий элемент символизирует ваш собственный модель. Мы берем во внимание все ваши пожелания, чтобы осуществить ваш дом еще еще больше дружелюбным и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]https://ppu-prof.ru[/url]

Не откладывайте занятия о своем жилище на потом! Обращайтесь к квалифицированным работникам, и мы сделаем ваш корпус не только теплым, но и более элегантным. Заинтересовались? Подробнее о наших делах вы можете узнать на нашем сайте. Добро пожаловать в пространство удобства и уровня.

Наша бригада опытных мастеров предоставлена предъявить вам перспективные системы, которые не только предоставят надежную защиту от прохлады, но и подарят вашему собственности стильный вид.

Мы работаем с последовательными строительными материалами, утверждая прочный срок службы службы и превосходные итоги. Утепление фасада – это не только экономия на обогреве, но и заботливость о окружающей природе. Энергоспасающие инновации, какие мы производим, способствуют не только своему, но и сохранению природных ресурсов.

Самое важное: [url=https://ppu-prof.ru/]Утепление стен снаружи услуги[/url] у нас открывается всего от 1250 рублей за кв. м.! Это доступное решение, которое переделает ваш помещение в подлинный теплый район с минимальными затратами.

Наши труды – это не только утепление, это создание площади, в котором всякий деталь преломляет ваш собственный манеру. Мы учтем все все твои требования, чтобы переделать ваш дом еще еще больше дружелюбным и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]www.ppu-prof.ru[/url]

Не откладывайте занятия о своем квартире на потом! Обращайтесь к профессионалам, и мы сделаем ваш дворец не только более теплым, но и по последней моде. Заинтересовались? Подробнее о наших сервисах вы можете узнать на веб-сайте. Добро пожаловать в универсум спокойствия и стандартов.

Customize your hero and embark on a thrilling quest! Lucky cola

Birçok sitede kandırıldım ama burada ne gördüysem onu yaşadım. AnkaraRusModel, Ankara escort hizmetinde kaliteyi temsil ediyor.

Yenimahalle, Etlik, Sincan gibi merkez dışı bölgelerde bile kaliteli escort profilleri görmek şaşırtıcıydı. Ankara escort ağını iyi kurmuşlar.

Çankaya’da bir süredir aradığım kaliteli ve güvenilir deneyimi nihayet bu sitede buldum. Çankaya escort arayanlara kesinlikle tavsiye ediyorum.

Her profilde özen ve kaliteyi görmek mümkün. Ankara Escort sektöründe gerçekten fark yaratıyorlar.

Explore the ranked best online casinos of 2025. Compare bonuses, game selections, and trustworthiness of top platforms for secure and rewarding gameplaycasino bonus.

Boy ve Kilo Ölçerler kategorisinden alışveriş yaptım. Boy ve Kilo Ölçerler ürünleri kaliteli, hızlı kargolu ve kullanışlı. Tavsiye ederim.

Zudem könnt ihr euer Glück noch an sieben Blackjack- und zehn Pokertischen, an denen die Gäste ausschließlich gegeneinander zocken, probieren. Ganz in der Nähe der Ruhrmetropole Dortmund und nur einen Steinwurf von der Burg Hohensyburg entfernt zieht die zur Westspiel-Gruppe gehörenden Spielbank seit 1985 Casino-Fans in seinen Bann. Zum Automatenspiel kann hingegen auch im legeren Look erschienen werden. Die Raucherbereiche sind ebenfalls klimatisiert und sind außerdem mit Spieltischen und Automaten ausgestattet, sodass auch während des Spielens rauchen möglich ist. Um das leibliche Wohl der Besucher wird sich in den attraktiven Barbereichen des Casinos gesorgt, die sowohl im Klassischen Spiel als auch im Automatensaal zu finden sind. Auf Automatenspiel muss nicht verzichtet werden, das sehr gut vom Klassischen Spiel getrennt wurde.

Selbst unerfahrene Spieler finden hier angemessene Veranstaltungen. Im Automatenspiel erfüllt ihr indes mit gepflegter Freizeitkleidung, die aber nicht zu leger gewählt werden sollte, die Kleidervorgaben. Das Rauchen an den Spieltischen ist in diesem Casino verboten, allerdings besteht im Automatenbereich Vegas World die Möglichkeit für eine Kippen-Pause. Das ist vornehmlich den vielen und regelmäßig stattfindenden Turnieren geschuldet, da auf diese Weise den Spielern und Zuschauern ein angenehmeres Umfeld geschaffen wird.

References:

https://online-spielhallen.de/mr-bet-casino-freispiele-ihr-schlussel-zu-mehr-spielspas/

You can reach the team via email, and VIP players also get a dedicated manager for tailored help. Huge pokies and live catalogue from Evolution, Pragmatic Play, Play’n GO, Nolimit City, Playtech, Ezugi Instant deposit; withdrawals to Paysafe where available Navigation is clean, mobile is slick, and payouts are quick once you’re verified. You get clear bonus rules, responsible play tools, and VIP care when you climb the levels. If you’re an Aussie looking for a fast, friendly place to play, this site keeps things simple.

Independent https://blackcoin.co/woo-casino-review-all-games-promotions/ sites also rank it among the most trusted options for Aussie players. For players in Woo Casino Australia, that level of transparency makes it easy to focus on the fun, knowing your data is locked down tight. Safety isn’t optional – it’s built into the core of Woo Casino online. With the right Woo Casino promo code, players unlock tailored offers that add even more value to their sessions.

Whether you’re playing a few pokies or going big at the live tables, payouts are transparent and on time. Money matters, and Woo Casino Australia makes sure deposits and payouts are simple, secure, and fast. Whether it’s pokies, jackpots, or classic tables, the sheer variety of Woo Casino games makes sure no session ever feels the same. The speed shows in instant crypto withdrawals and fast banking options in AUD, so players don’t get stuck waiting for their winnings. The casino also supports both cash and crypto, with a clean interface that keeps banking and games easy to find.

online casino that accepts paypal

References:

http://asianmate.kr/bbs/board.php?bo_table=free&wr_id=1085617

online casino with paypal

References:

https://uaslaboratory.synology.me/gnu5/bbs/board.php?bo_table=free&wr_id=1908562

**mitolyn**

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

Новейшие сайты для взрослых предлагают инновационный контент для развлечений для

взрослых. Откройте для себя гарантированные

порнохабы для современного опыта.

my web page: Buy Rivotril

Лучшие xxx сайты предоставляют премиум-контент

для зрелой аудитории. Исследуйте надежные источники для качества и конфиденциальности.

My web site; buy viagra online

Взрослый контент доступны на различных сайтах для

взрослых в развлекательных целях.

Всегда выбирайте защищенные центры контента

для защищенного опыта.

Here is my blog post; купить валиум онлайн

Смотрите видео для взрослых на безопасных и надежных платформах.

Найдите гарантированные источники видео для первоклассного опыта.

Feel free to visit my blog :: buy viagra online

Найдите контент для взрослых, исследуя надежные платформы в

Интернете. Изучите защищенные источники контента для приватного просмотра.

Feel free to surf to my homepage :: ebony porn

Контент для взрослых доступен через гарантированные веб-сайты.

Изучите надежные источники для получения

качественного контента.

My page :: DOWNLOAD TOP PORN VIDEOS

Лучшие xxx сайты предоставляют премиум-контент для зрелой аудитории.

Исследуйте надежные источники для качества и конфиденциальности.

Have a look at my homepage; orgy porn videos

Ведущие порносайты предоставляют премиум-контент для зрелой аудитории.

Исследуйте безопасные хабы для

качества и конфиденциальности.

Feel free to visit my website; BUY RIVOTRIL

Новые порносайты предлагают инновационный контент для

развлечений для взрослых.

Откройте для себя безопасные новые платформы

для современного опыта.

Also visit my web page; купить травку

Ищите откровенные видео,

исследуя надежные платформы

в Интернете. Изучите безопасные сайты для приватного просмотра.

Найдите контент для взрослых, исследуя надежные

платформы в Интернете. Изучите

защищенные источники контента

для приватного просмотра.

Топовые сайты для взрослых предлагают высококачественный

контент для взрослых развлечений.

Выбирайте безопасные сайты

для безопасного и приятного

просмотра.

My homepage … BRAND NEW PORN SITE SEX

Контент для взрослых доступен

через надежные и проверенные веб-сайты.

Изучите надежные источники для получения

качественного контента.

My web blog: КУПИТЬ АДДЕРАЛЛ ОНЛАЙН БЕЗ РЕЦЕПТА

Ищите откровенные видео, исследуя надежные платформы в Интернете.

Изучите безопасные сайты для приватного просмотра.

Here is my web site; watch top porn videos

Порно доступны на различных сайтах для взрослых в развлекательных целях.

Всегда выбирайте защищенные центры контента для защищенного

опыта.

my web site: BUY VALIUM ONLINE

Просматривайте откровенные материалы купить Аддералл онлайн без рецептаопасно, выбирая проверенные веб-сайты для взрослых.

Используйте надежные порнохабы

для конфиденциального развлечения.

Материалы для взрослых доступны на различных сайтах для взрослых в развлекательных целях.

Всегда выбирайте безопасные платформы для защищенного опыта.

Feel free to surf to my webpage buy viagra

Найдите контент для взрослых, исследуя надежные платформы в Интернете.

Изучите безопасные сайты для приватного просмотра.

Also visit my web blog – BUY RIVOTRIL

Backbiome is an advanced daily wellness supplement formulated to help support spinal comfort, reduce feelings of built-up tension, and promote freer, smoother movement throughout backbiome everyday life.

Контент для взрослых доступен через надежные и проверенные

веб-сайты. Изучите безопасные сайты для взрослых для получения качественного контента.

My website – купить каннабис онлайн

Найдите контент для взрослых,

исследуя надежные платформы в Интернете.

Изучите надежные порнохабы

для приватного просмотра.

Here is my web blog: BUY CANNABIS ONLINE

Транслируйте контент для взрослых безопасно, выбирая проверенные веб-сайты для взрослых.

Используйте надежные порнохабы для конфиденциального развлечения.

Check out my page; купить травку

Где смотреть порно, исследуя надежные платформы в Интернете.

Изучите безопасные сайты для приватного просмотра.

Here is my web blog – best anal porn site

We recognize the value of your time, which is why

we have incorporated a Turbo Mode feature into Easy Videos Downloader.